- The mood at last week’s Miami Boat Show was sunny, like the weather. Enthusiastic shoppers, lots of shiny new boats, and based on conversations with manufacturers, not enough new boats to meet demand.

However, as previously posted, some clouds on the horizon foreshadow the powerboat industry’s vulnerability in a way that will redefine the landscape over the next 10 years.

- The core buyer base is aging. The 55-60 year old buyer base (let’s generalize and call them Boomers), are committed and usually repeat buyers. And they look a lot alike (in the words of one industry executive: “pale, stale and male”).

But there aren’t enough younger first-time buyers (generalized as Millennials) to replace their unit or dollar sales. Over the last 15+ years, the share of new boats sold to first-time buyers has dropped dramatically.

It’s the same old dudes buying more boats. - Recession bites. The next recession, like the last one, will flood the market with used boats when owners sell, crushing new boat sales – – a sales circuit-breaker if enough Boomer owners exit the market permanently. Remember, older buyers generally buy the more expensive boats.

Typical core new boat buyer

This post tries to explain why there are not enough younger boat buyers, and offers some ideas of what can be done to prepare for the future. While a bit longer than my typical post, there are lots of pictures, so please read on.

Source: NMMA

Following our Miami visit we circled back to get input from senior leaders representing manufacturers, dealers, Freedom Boat Club (the leader in this segment) and the NMMA, the leading trade association.

The upshot: the core appeal of powerboating is not going anywhere, but the industry will need structural changes to address some fairly major challenges to sustain health (read: sales) over the long term.

And the current pace of innovation is not enough to drive the changes necessary. Disruptive innovation is needed in everything from boat design, mode of power, sales/distribution channels to marketing. This is not about reducing price or offering new colors or more horsepower.

Disruptors transform the way a basic demand is delivered. Myopia has led to the downfall of many former market leaders.

- Home Video: Blockbuster (VHS/DVD) yields to Netflix (streaming)

- Personal photography: Kodak (film) yields to digital / smartphones

- Books: Borders (bricks & mortar) yields to Amazon (online)

Based on appearances, the powerboat industry seems headed this direction – – focused on maximizing revenue with the current model (largely fiberglass gas-powered outboard boats sold through dealers).

There are signs that disruptors are at work — but there is a long way to go.

![]()

To explain where the industry has been and where it needs to go, we compared the buying process of legacy (Boomer) core buyers with considerations of potential Millennial buyers, in a 4-step process.

So what are some paths to long-term growth?

Here are some ways the industry can take action (with some examples):

- Before addressing new buyers, the industry must keep current owners around as long as possible.

Slow down defections – – aggressively court current owners and build relationships through CRM, owner events and personal outreach – build loyalty and maybe get another purchase

To encourage Millennial first-time buyers:

INTEREST

- Accelerate development of more agreeable, alternative power sources:

- GM’s experimental marine division, Forward Marine, introduced a 100% battery-powered boat. With a max speed of 20mph and a range of 1 hour at that speed, it’s not ready for prime time yet, and won’t get you many dates, but this is the direction some of the industry will go. Think Tesla. Maybe a hybrid as well.

GM Forward Marine prototype

- Indmar just introduced EcoBoost, the marine version of Ford’s EcoTec engine – gets the same horsepower and torque with 4 cylinders as a typical V-8. More environmentally friendly.

Indmar EcoBoost

- Torqeedo is an established German company offering quiet, efficient electric motors. Due to relatively low gas prices and a maximum of 100 hp, growth is slow but it is steady. They’re getting traction.

Torqeedo Deep Blue 80R

- BlueGas Marine has developed economical natural gas power for boats. Traction is difficult for the above reasons as well as infrastructure (need the gas equivalent of charging stations), but the equation can change quickly if oil prices spike.

More aggressive marketing

- Cross-market! Boating should not just be for insiders anymore! Visibility must be increased by pursuing prospects with related affinities: skiing, hiking, etc. Not just a booth at the boat show.

- Be more inclusive, diverse and experiential. Feature a range of age, ethnicity, interests. Leverage social media to reach prospects beyond the familiar core demographics.

- Innovate beyond current offerings – materials, design, features

- New boaters don’t have the burden of tradition and will likely be more open to unconventional but more functional approaches (after all, someone had to buy the first Prius)

- RIBs – Rigid Inflatable Boats (Axopar, Technohull) offer more efficient performance using different hull design and materials. They are really cool, perform great, look different, and that’s ok.

Technohull (top); Axopar

- Powered catamarans look different but offer advantages of smooth ride and more space

EXPERIENCE

Leverage technology to reduce fear as a barrier to purchase

- Self-docking boats will be available in 2020

- On-board digital video tutorials can provide much more effective learning than paper manuals

- Controls are shifting from analog to digital, to mimic/integrate with smartphones

OWNERSHIP

- Offer more versatile/multi-use boats at attractive price points – not single purpose (e.g. fishing) but can handle a variety of activities on any given day (analog: SUVs), making purchase more acceptable

- Sea-Doo introduced a jet ski that converts to a fishing craft – – and it starts at $15k

- Yamaha’s 2018 Boat of the Year (the FSH 210) is an affordable, do-it-all boat that is an excellent choice for first-time boaters.

- Don’t require purchase to participate

- Freedom Boat Club is a franchisor with 178 locations, with a model based on eliminating some key barriers to purchase (includes lessons, takes care of maintenance and insurance). The goal – make participation frictionless.

- Members pay a monthly fee for unlimited access to a variety of boats in a huge number of locations, rather than committing 6-figures for a single boat.

![]()

- Other similar models such as peer-to-peer rental, fractional use, etc. will undoubtedly increase as there is less reliance on solely purchase

- More fully integrate the internet in the shopping/buying process – as in the auto industry, reduce reliance on aggressive final-mile dealer salespeople.

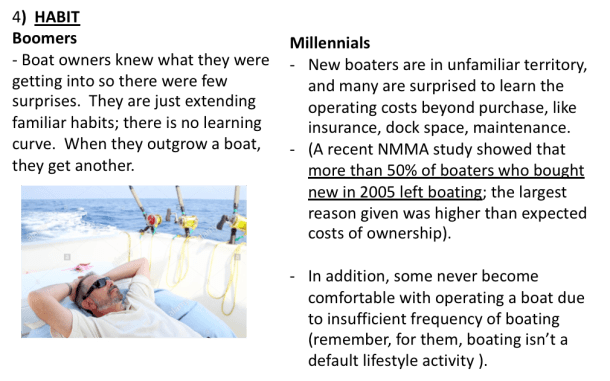

HABIT

No surprises!

- Full transparency in the sales process, specifically costs/ obligations of ownership

- Continuous on-boarding/learning from the dealer, not just 2 hours when the boat is picked up

- Aggressively encourage new boater networking to share tips, experiences, and create peer communities

- Mentoring programs linking experienced boaters with new boaters. Older boaters would love to pass along insights; a no-judgment setting makes it a win-win.

These are just a few things the industry can do to mitigate unavoidable changes. It will take foresight, patience, and investment – – and may not pay off immediately.

But an industry that proactively and creatively adapts to the needs of new boaters with great product and a great experience, will be much more successful than what we currently seem to have – – an industry that asks potential new buyers to adapt to the way things have been.